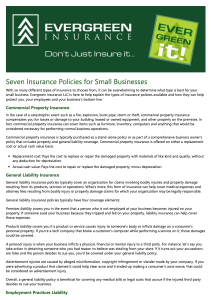

Happy National Small Business Day! Evergreen Insurance is here to support and help protect your small business from the risks and liabilities you may face. Choosing the right business insurance for your company can be overwhelming. Click on the image to download or print the sheet for details on different types of insurance.

Truck drivers face long hours and inclement weather when on the job. If your business employs independently contracted drivers, it’s smart to provide occupational accident coverage to help protect them and your company in the event of injury and accidents. Click on the image to download or print the sheet for more information.

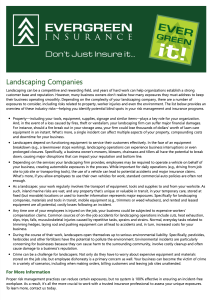

Landscaping can be a very successful business, but the risk exposures can be complex. To keep your landscaping organization running smoothly, you need to address the risks associated with property, injuries, and more. Click on the image to download or print a list of industry risks.

Does your property have a playground? Playgrounds are a great place for families with children of all ages. When owning and maintaining a playground, it is essential that you balance fun and safety in order to mitigate liability for the inevitable playground injuries. Click on the image to download or print the safety sheet.

Cybersecurity risks continue to expand nearly unabated. While it can feel like trying to hold back a tidal wave with a bath towel sometimes, effective tools do exist and can be easily accessed.

What must always be remembered is that a commitment to resilience and pre-emptive mitigation remains imperative. Insurers are well-positioned to serve not only as financial first responders but as partners in managing these evolving hazards, along with their business associates and partners.

According to the Insurance Information Institute, “The first line of defense is creating a robust cybersecurity system, training employees on how to identify a potential attack, encrypting company data, and enabling antivirus protection. With only half of businesses reporting a consistent encryption strategy, and the cost of data breaches continuing to rise, organizations must do more to protect themselves and their customers.”.

Some commonly seen cyber liability risks include:

Liability—You may be liable for costs incurred by customers and other third parties as a result of a cyber attack or other IT-related incident.

System recovery—Repairing or replacing computer systems or lost data can result in significant costs.

Notification expenses—In several states, if your business stores customer data, you’re required to notify customers if a data breach has occurred or is even just suspected.

Regulatory fines—Several federal and state regulations require businesses and organizations to protect consumer data.

Class action lawsuits—Large-scale data breaches have led to class action lawsuits filed on behalf of customers whose data and privacy were compromised.

To extend cyber liability insurance coverage requires the purchase a stand-alone cyber liability policy, customized for your business to cover several types of risk, including:

Loss or corruption of data.

Business interruption.

Multiple types of liability.

Identity theft.

Cyber extortion.

Reputation recovery.

Contact the professionals at Evergreen for more information and guidance on obtaining the proper level of cyber liability insurance coverage for your situation.

Copyright 2023 Evergreen Insurance

Evergreen Insurance provides these updates for information only, and does not provide legal advice. To make decisions regarding insurance matters, please consult directly with a licensed insurance professional or firm.

Securing appropriate insurance for your business and property can be enough of a process on its own. So what does the concept of coinsurance represent? Nothing less than protection for both the insured and the insurance provider.

Let’s start with defining our terms. Coinsurance is a property coverage provision set by your insurer that requires you to carry coverage for a certain percent of your property’s value. That way, your insurer can be sure you have adequate coverage if you need to make a claim, and it can ensure that its resources are adequate to cover that claim.

In a typical commercial property insurance policy, a coinsurance clause ensures that you carry adequate coverage to protect your assets. For instance, for an office building valued at $200,000, you would need at least $200,000 in property insurance coverage. If your policy has a clause with a coinsurance percentage of at least 80%, that means you must insure the building for at least $160,000. If you purchase less coverage, the insurance company may not pay out the full value of your damages, even if they fall within the limits of your policy.

Say you file a claim after a fire causes $100,000 worth of property damage. Your property insurance policy has a limit of $150,000 and a $5,000 deductible. Per your coinsurance clause, you were required to purchase at least $160,000 in coverage. Because you failed to meet your coinsurance percentage of 80%, you will face additional costs as determined by the ratio of the amount you carried divided by the amount that was required: $150,000 / $160,000 = 0.937. So if your loss was $100,000, your insurer will pay $93,700 minus your $5,000 deductible. Your total costs will end up being $11,300.

Not every insurance company includes a coinsurance clause in its policies. However, those that do require coinsurance typically have three reasons for doing so:

To ensure clients have adequate coverage.

To protect their pool of resources to better handle real-world claim situations.

To encourage accurate assessment and underwriting.

The bottom line? When you’re required to meet coinsurance limits and do so, you’re more likely to make an accurate assessment of the value of your assets, which protects the insurance provider and you in the long term. Contact the professionals at Evergreen for more information on coinsurance and how it can apply to your business coverage.

Copyright 2023 Evergreen Insurance

Evergreen Insurance provides these updates for information only, and does not provide legal advice. To make decisions regarding insurance matters, please consult directly with a licensed insurance professional or firm.

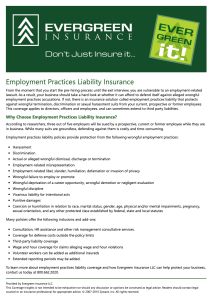

Employee-related lawsuits can be time-consuming and costly for your business. Employment practices liability insurance can help shield your business from these suits. What does this liability insurance cover? Click on the image to download or print the information sheet.

A sharp rise in the number and size of ransomware losses over the past three years is changing the availability and cost of cybersecurity insurance coverage, according to the Insurance Leadership Forum. Annual cyber liability rates have increased more than 40% in recent years, in fact.

Insurance providers are carefully managing the growing risk, with some scaling back coverage options for business customers and others continuing to make coverage widely available because the threat is both ever-present, growing and evolving rapidly.

Some insurers continue to make this coverage available to customers with whom they have a wider relationship. Certain insurers have elected to only write cyber liability for companies with less than $100 million in revenue to reduce the insurer’s exposure.

These factors combine to make the need for cybersecurity insurance more urgent than ever, and to secure adequate coverage at reasonable rates. Contact the professionals at Evergreen to learn more about available cybersecurity coverage that’s right for your business.

Copyright 2023 Evergreen Insurance

Evergreen Insurance provides these updates for information only, and does not provide legal advice. To make decisions regarding insurance matters, please consult directly with a licensed insurance professional or firm.

Floods, fires, tornadoes. Business owners purchase insurance to protect their property and people against these types of disasters. But what happens when, should the worst occur, you can’t adequately prove what that property was worth, or the financial impact your people are suffering?

It may sound like the most obvious point in the world, but it’s important to have accurate values – and the documentation to prove them to an insurance adjuster. Some good news is that this is not so much an issue impacting your premiums, but it can become a major issue when filing a claim to recover your losses.

The Insurance Information Institute recommends the following:

— Collect any relevant business records that you will need to prove the value of damaged equipment, inventory or structures that you are including in your business insurance claim. Gather all financial documents including tax returns, monthly sales tax returns, business contracts, budgets, financial statements and other documents pertinent to calculating the projected income of your business.

— If the business is forced to close down, you will need to provide information on the cost of conducting business from a temporary location, detailed records of business activity, and a list of expenses that have continued while your business has been suspended such as advertising, utilities, etc. Loss of or damage to cars, vans, trucks or specialty vehicles, which can hamper your ability to operate your business, should also be reported.

One of the smartest and easiest ways for a business owner to limit risk is to make sure you know – and can prove – what the various elements that make up your business are worth.

Contact the professionals at Evergreen to learn more about insured-to-value coverage for your enterprise.

Copyright 2023 Evergreen Insurance

Evergreen Insurance provides these updates for information only, and does not provide legal advice. To make decisions regarding insurance matters, please consult directly with a licensed insurance professional or firm.

In life, as in business, education, and any large organization, the only thing that doesn’t change is that everything changes.

New operational subsidiaries are formed, people in key leadership positions leave and arrive, school districts see new clubs and sports teams rise and fall. Nothing wrong with any of this. It’s the natural ebb and flow. It’s how the world works.

The sticky part comes in, however, when you assume the insurance coverage in place extends to any or all of those modifications. Or worse, you don’t think of that question at all.

The old adage about why it’s dangerous to assume certainly applies. A policy is written at a moment in time, under specifications and structures that exist then. Unless provisions have been written into that policy to automatically include new elements to the entity being covered, they may not – and probably will not.

Always err on the side of caution and communication. Check with your insurance provider any time the terms, shape, size, or any other variable impacts your organization. When changes are afoot, make sure you know who and what is covered under your policy – so that any necessary adjustments can be made before costly surprises arise.

Contact the professionals at Evergreen for more information.

Copyright 2022 Evergreen Insurance

Evergreen Insurance provides these updates for information only, and does not provide legal advice. To make decisions regarding insurance matters, please consult directly with a licensed insurance professional or firm.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.